Estimates from Sample Covariance

Contents

Estimates from Sample Covariance¶

The portfolios we constructed in this notebook serve as reference to the portfolios using cosine similarity estimates and factor model estimates. Here, we simply use the sample return and sample covariance to generate portfolios for each industry.

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns

r_selected = pd.read_csv("data/filtered_r.csv")

# get the mean of all

r_selected.set_index("name", inplace = True)

mu = r_selected.mean(axis = 1)

# compute the covariance matrix

cov = r_selected.T.cov()

Perform Mean-Variance Analysis¶

We will use one industry per time to generate a minimum-variance portfolio. In our demonstration of mean-variance analysis process, we use the industry pharmaceutical preparations whose SIC code is 2834. At the end, we will show the results for other industries.

We first get the name list of pharmaceutical preparations companies and match the names with the companies in returns data. Then, we get the sample mean and sample covariance for this specific industry. We get the efficient frontier, the set of optimal portfolios, for the industry; and recognize the minimum-variance portfolio with its performance and its weights for selected companies.

from pypfopt import EfficientFrontier

from pypfopt import risk_models

from pypfopt import expected_returns

from pypfopt import objective_functions

from pypfopt import plotting

df = pd.read_csv('../data/preprocessed.csv',

usecols = ['reportingDate', 'name', 'CIK',

'coDescription_stopwords', 'SIC', 'SIC_desc'])

df = df.set_index(df.name)

# get the names of the companies in the pharmaceutical preparations industry

Pharm = df[df.SIC == 2834]

Pharm_list = Pharm.index

# get the companies name that match return data and business description data

SET = (set(Pharm_list) & set(r_selected.index))

LIST = [*SET, ]

Sample Mean for the Pharmaceutical Preparations Industry¶

name

ALEXION PHARMACEUTICALS INC -0.007589

VALEANT PHARMACEUTICALS INTERNATIONAL, INC. 0.004328

ARENA PHARMACEUTICALS INC 0.032450

THERAPEUTICSMD, INC. -0.016246

XENCOR INC 0.040986

...

PFIZER INC 0.011145

TONIX PHARMACEUTICALS HOLDING CORP. -0.091454

ENANTA PHARMACEUTICALS INC 0.043121

SYNTHETIC BIOLOGICS, INC. -0.117010

PROTHENA CORP PLC -0.022615

Length: 124, dtype: float64

Sample Covariance for the Pharmaceutical Preparations Industry¶

| name | ALEXION PHARMACEUTICALS INC | VALEANT PHARMACEUTICALS INTERNATIONAL, INC. | ARENA PHARMACEUTICALS INC | THERAPEUTICSMD, INC. | XENCOR INC | AKORN INC | CONCERT PHARMACEUTICALS, INC. | AMICUS THERAPEUTICS INC | MERCK & CO., INC. | RXI PHARMACEUTICALS CORP | ... | PACIRA PHARMACEUTICALS, INC. | RETROPHIN, INC. | WAVE LIFE SCIENCES LTD. | SERES THERAPEUTICS, INC. | ATHERSYS, INC / NEW | PFIZER INC | TONIX PHARMACEUTICALS HOLDING CORP. | ENANTA PHARMACEUTICALS INC | SYNTHETIC BIOLOGICS, INC. | PROTHENA CORP PLC |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| name | |||||||||||||||||||||

| ALEXION PHARMACEUTICALS INC | 0.012712 | 0.006660 | 0.006930 | 0.005225 | 0.001170 | 0.007724 | -0.001042 | 0.006752 | 0.000882 | -0.002845 | ... | 0.003835 | 0.004225 | -0.003400 | 0.005804 | 0.001423 | 0.001644 | -0.000341 | 0.004035 | 0.007318 | 0.004338 |

| VALEANT PHARMACEUTICALS INTERNATIONAL, INC. | 0.006660 | 0.039376 | 0.009791 | 0.013252 | 0.001746 | 0.003388 | -0.000155 | 0.008508 | 0.003592 | 0.005348 | ... | 0.014738 | -0.001323 | 0.006341 | 0.008791 | 0.004323 | 0.001972 | 0.018120 | 0.002381 | 0.003896 | 0.000611 |

| ARENA PHARMACEUTICALS INC | 0.006930 | 0.009791 | 0.016468 | 0.009590 | 0.005659 | 0.003093 | 0.002774 | 0.008793 | -0.000367 | 0.007589 | ... | -0.001459 | 0.006164 | 0.004010 | 0.009748 | 0.003847 | 0.000946 | -0.000497 | 0.006247 | 0.008589 | 0.004414 |

| THERAPEUTICSMD, INC. | 0.005225 | 0.013252 | 0.009590 | 0.022313 | 0.005284 | 0.005202 | 0.012489 | 0.005136 | 0.001250 | 0.014646 | ... | 0.008701 | 0.006256 | 0.012576 | 0.015942 | 0.011200 | 0.002476 | 0.008163 | 0.006193 | 0.002654 | 0.000172 |

| XENCOR INC | 0.001170 | 0.001746 | 0.005659 | 0.005284 | 0.022963 | 0.000706 | 0.003764 | -0.000624 | 0.000666 | 0.005584 | ... | -0.001834 | 0.006962 | 0.013082 | 0.010240 | 0.003081 | 0.001374 | -0.000513 | 0.002233 | -0.001098 | 0.002824 |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| PFIZER INC | 0.001644 | 0.001972 | 0.000946 | 0.002476 | 0.001374 | 0.002698 | 0.000957 | 0.000309 | 0.000939 | 0.000719 | ... | 0.002475 | 0.001162 | 0.001007 | 0.001630 | 0.002291 | 0.001698 | -0.000593 | 0.000069 | 0.000604 | 0.001456 |

| TONIX PHARMACEUTICALS HOLDING CORP. | -0.000341 | 0.018120 | -0.000497 | 0.008163 | -0.000513 | 0.002554 | 0.003213 | 0.005606 | 0.000483 | -0.004720 | ... | 0.004383 | -0.004944 | -0.003492 | 0.009418 | -0.000825 | -0.000593 | 0.065843 | 0.007495 | 0.007087 | 0.000283 |

| ENANTA PHARMACEUTICALS INC | 0.004035 | 0.002381 | 0.006247 | 0.006193 | 0.002233 | 0.006631 | 0.003183 | 0.005128 | 0.000286 | 0.004438 | ... | -0.004859 | 0.008284 | 0.000024 | 0.007459 | 0.003778 | 0.000069 | 0.007495 | 0.019068 | 0.006687 | 0.005810 |

| SYNTHETIC BIOLOGICS, INC. | 0.007318 | 0.003896 | 0.008589 | 0.002654 | -0.001098 | 0.017232 | -0.003878 | 0.012808 | -0.000625 | 0.003202 | ... | -0.002593 | 0.007492 | -0.001993 | 0.005251 | 0.008775 | 0.000604 | 0.007087 | 0.006687 | 0.047660 | 0.009052 |

| PROTHENA CORP PLC | 0.004338 | 0.000611 | 0.004414 | 0.000172 | 0.002824 | 0.016777 | 0.005445 | 0.015848 | 0.000710 | 0.011297 | ... | 0.000575 | 0.007092 | -0.005593 | -0.006159 | 0.005641 | 0.001456 | 0.000283 | 0.005810 | 0.009052 | 0.043454 |

124 rows × 124 columns

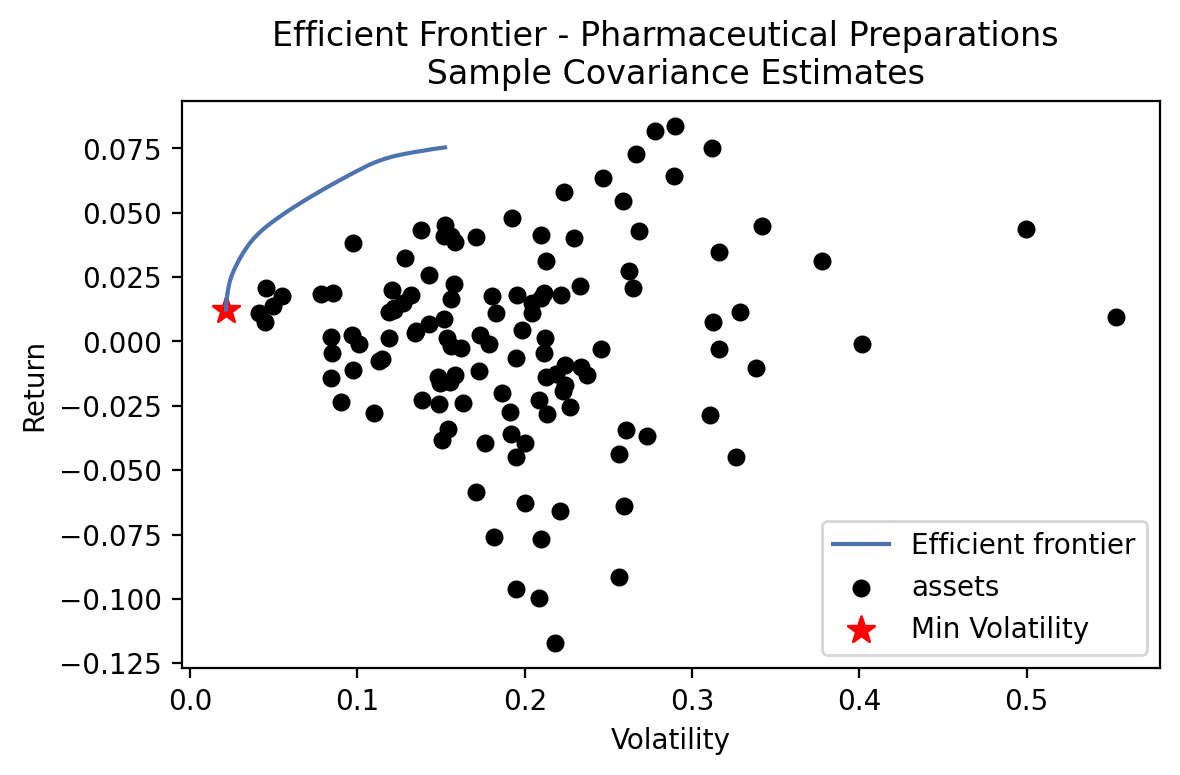

Efficient Frontier - Pharmaceutical Preparations¶

ef1 = EfficientFrontier(mu_Pharm, cov_Pharm, weight_bounds=(0, 0.2))

fig, ax = plt.subplots()

plotting.plot_efficient_frontier(ef1, ax=ax, show_assets=True)

# Find and plot the tangency portfolio

ef2 = EfficientFrontier(mu_Pharm, cov_Pharm, weight_bounds=(0, 0.2))

# min volatility

ef2.min_volatility()

ret_tangent, std_tangent, _ = ef2.portfolio_performance()

ax.scatter(std_tangent, ret_tangent, marker="*", s=100, c="r", label="Min Volatility")

# Format

ax.set_title("Efficient Frontier - Pharmaceutical Preparations \n Sample Covariance Estimates")

ax.legend()

plt.tight_layout()

plt.savefig('images/Efficient_Frontier_Sample_Pharmaceutical_Preparations.png', dpi=200, bbox_inches='tight')

plt.show()

Min Volatility Portfolio¶

Performance¶

ef2.portfolio_performance(verbose=True);

Expected annual return: 1.2%

Annual volatility: 2.1%

Sharpe Ratio: -0.35

Weights¶

companies = []

weights = []

for company, weight in ef2.clean_weights().items():

if weight != 0:

companies.append(company)

weights.append(weight)

dic = {'Company_Name':companies,'Weight':weights}

min_vol = pd.DataFrame(dic)

min_vol.to_csv("data/min_vol_sample_Pharmaceutical_Preparations.csv", index = False)

pd.read_csv("data/min_vol_sample_Pharmaceutical_Preparations.csv")

| Company_Name | Weight | |

|---|---|---|

| 0 | MERCK & CO., INC. | 0.20000 |

| 1 | ACHAOGEN INC | 0.00515 |

| 2 | BRISTOL MYERS SQUIBB CO | 0.12824 |

| 3 | PROPHASE LABS, INC. | 0.05120 |

| 4 | HEAT BIOLOGICS, INC. | 0.00297 |

| 5 | CHEMBIO DIAGNOSTICS, INC. | 0.02843 |

| 6 | ORAMED PHARMACEUTICALS INC. | 0.04982 |

| 7 | ASSEMBLY BIOSCIENCES, INC. | 0.05775 |

| 8 | IMPRIMIS PHARMACEUTICALS, INC. | 0.04181 |

| 9 | MANNKIND CORP | 0.02048 |

| 10 | ARATANA THERAPEUTICS, INC. | 0.03678 |

| 11 | PFENEX INC. | 0.03777 |

| 12 | STEMLINE THERAPEUTICS INC | 0.04273 |

| 13 | RECRO PHARMA, INC. | 0.02010 |

| 14 | LIPOCINE INC. | 0.00683 |

| 15 | JOHNSON & JOHNSON | 0.17878 |

| 16 | BIODELIVERY SCIENCES INTERNATIONAL INC | 0.03680 |

| 17 | XENON PHARMACEUTICALS INC. | 0.01350 |

| 18 | ZOETIS INC. | 0.01195 |

| 19 | VTV THERAPEUTICS INC. | 0.02372 |

| 20 | CYTOMX THERAPEUTICS, INC. | 0.00520 |

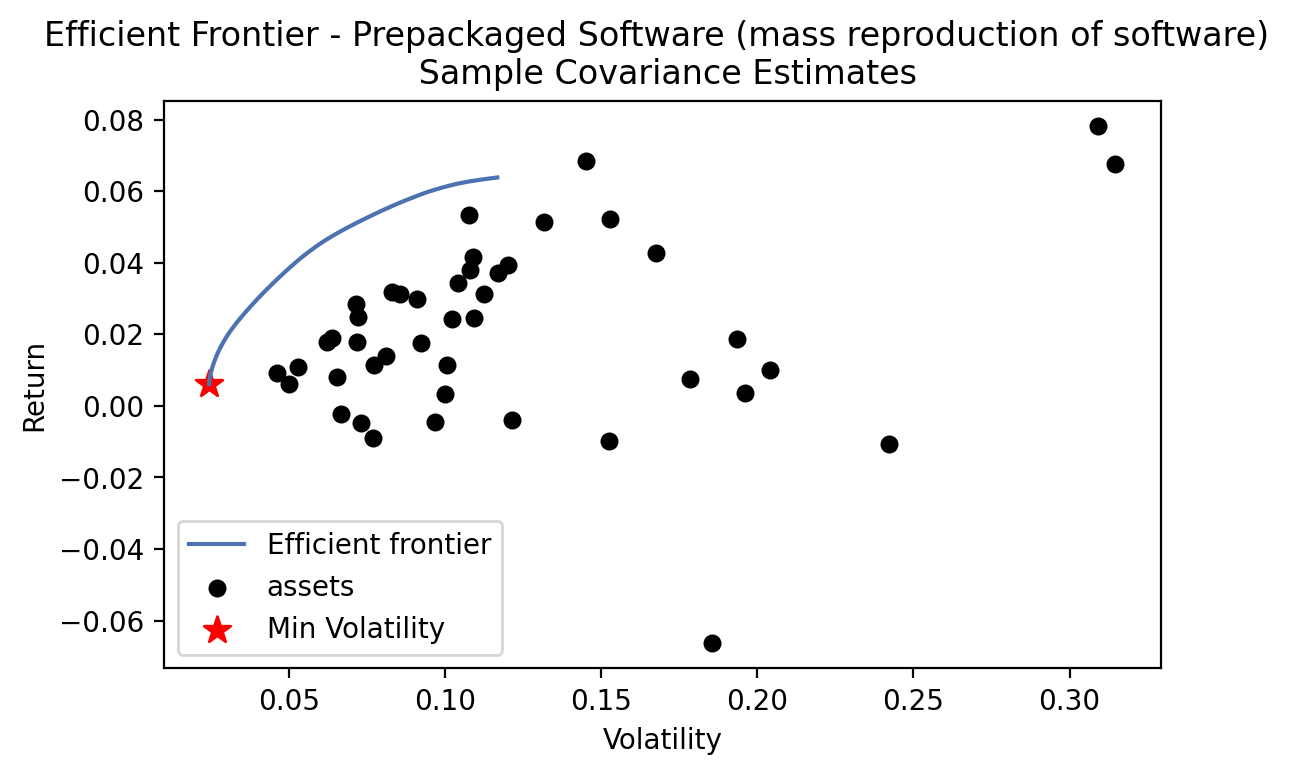

Results for the Other 4 Industries¶

Prepackaged Software (mass reproduction of software)¶

Min Volatility Portfolio¶

Performance¶

Expected annual return: 0.6%

Annual volatility: 2.4%

Sharpe Ratio: -0.57

Weights¶

| Company_Name | Weight | |

|---|---|---|

| 0 | ORACLE CORP | 0.09170 |

| 1 | AVID TECHNOLOGY, INC. | 0.00129 |

| 2 | ZEDGE, INC. | 0.01792 |

| 3 | MAJESCO | 0.01906 |

| 4 | MICROSTRATEGY INC | 0.02160 |

| 5 | NUANCE COMMUNICATIONS, INC. | 0.08608 |

| 6 | QUMU CORP | 0.05153 |

| 7 | BLACK KNIGHT, INC. | 0.20000 |

| 8 | QUALYS, INC. | 0.06668 |

| 9 | AWARE INC /MA/ | 0.20000 |

| 10 | ENDURANCE INTERNATIONAL GROUP HOLDINGS, INC. | 0.02554 |

| 11 | LIVEPERSON INC | 0.01519 |

| 12 | COMMVAULT SYSTEMS INC | 0.07381 |

| 13 | ROSETTA STONE INC | 0.01647 |

| 14 | ACI WORLDWIDE, INC. | 0.11314 |

Crude Petroleum and Natural Gas¶

When we conduct the same analysis, there is no weight shown. Efficient frontier cannot be found.

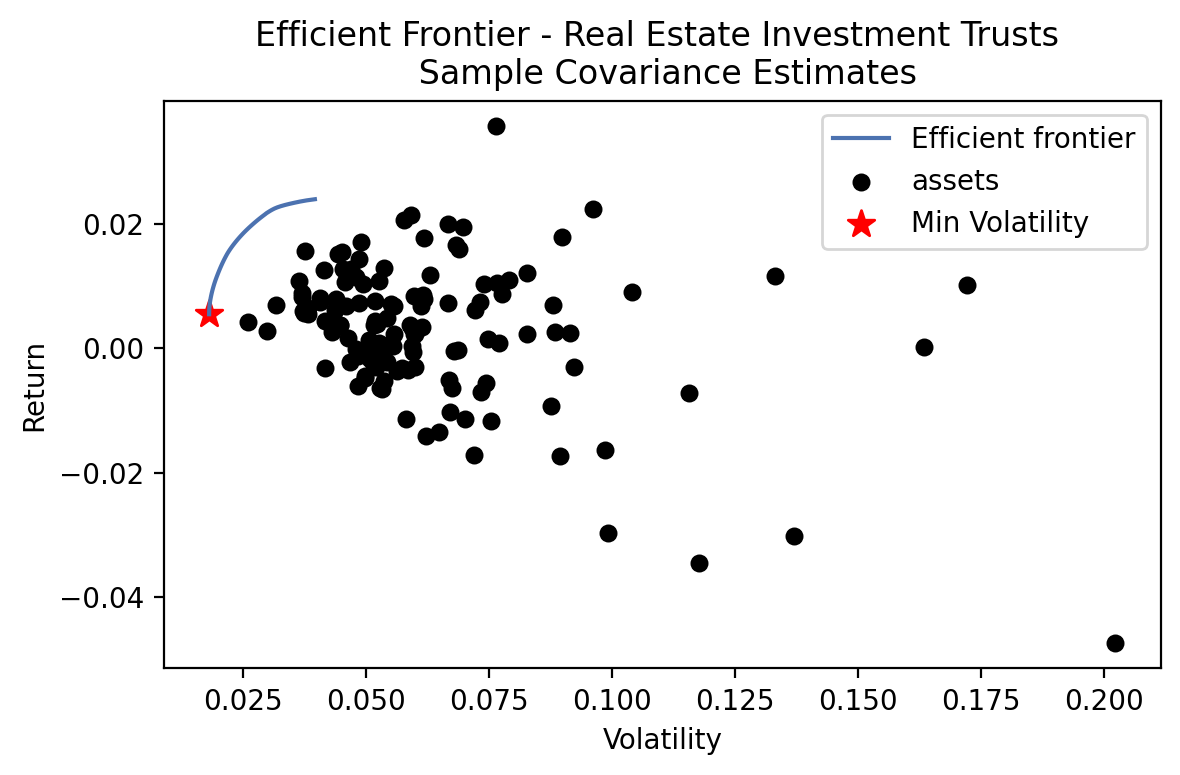

Real Estate Investment Trusts¶

Min Volatility Portfolio¶

Performance¶

Expected annual return: 0.5%

Annual volatility: 1.8%

Sharpe Ratio: -0.80

Weights¶

| Company_Name | Weight | |

|---|---|---|

| 0 | PUBLIC STORAGE | 0.10950 |

| 1 | GREAT AJAX CORP. | 0.20000 |

| 2 | CIM COMMERCIAL TRUST CORP | 0.05453 |

| 3 | MANHATTAN BRIDGE CAPITAL, INC | 0.01480 |

| 4 | BRT APARTMENTS CORP. | 0.01720 |

| 5 | ALEXANDERS INC | 0.02292 |

| 6 | LADDER CAPITAL CORP | 0.04406 |

| 7 | NEW YORK MORTGAGE TRUST INC | 0.02065 |

| 8 | ARES COMMERCIAL REAL ESTATE CORP | 0.09123 |

| 9 | CROWN CASTLE INTERNATIONAL CORP | 0.04853 |

| 10 | IMPAC MORTGAGE HOLDINGS INC | 0.05104 |

| 11 | HMG COURTLAND PROPERTIES INC | 0.12520 |

| 12 | EQUITY COMMONWEALTH | 0.20000 |

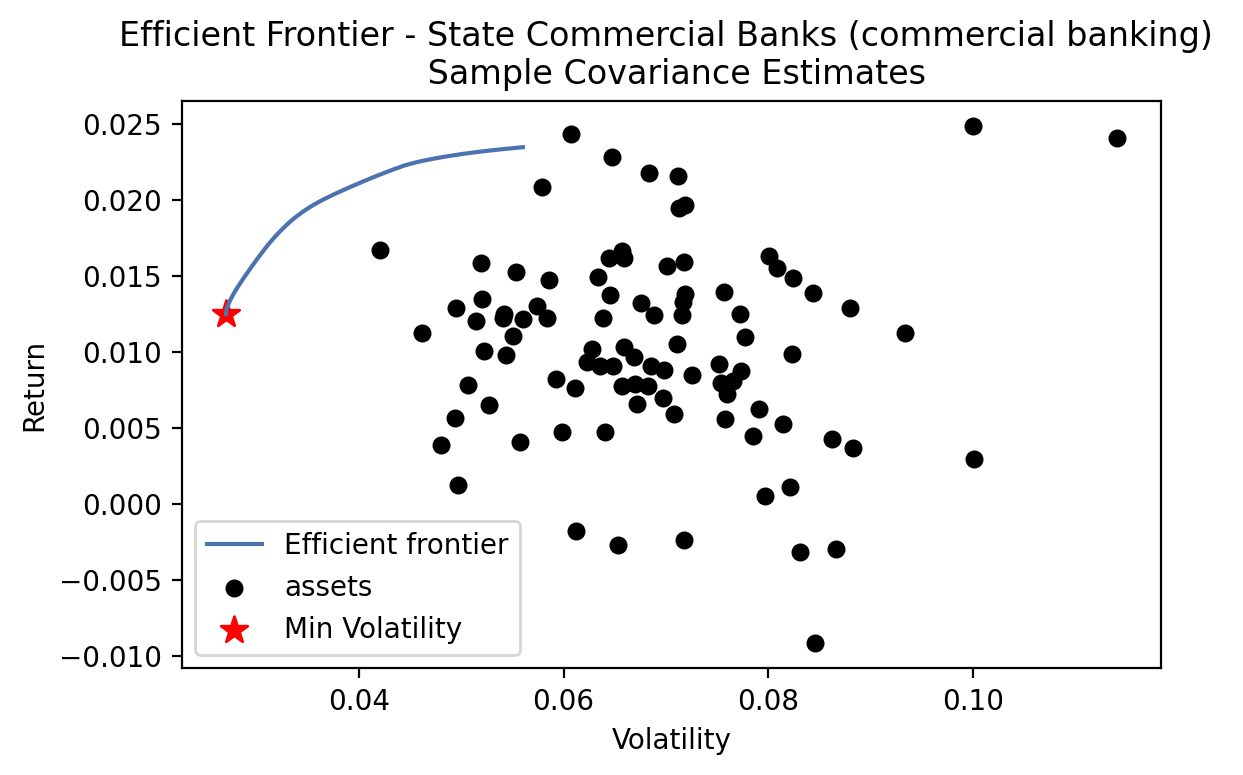

State Commercial Banks (commercial banking)¶

Min Volatility Portfolio¶

Performance¶

Weights¶

| Company_Name | Weight | |

|---|---|---|

| 0 | RELIANT BANCORP, INC. | 0.12273 |

| 1 | CAROLINA TRUST BANCSHARES, INC. | 0.11786 |

| 2 | BANK OF THE JAMES FINANCIAL GROUP INC | 0.00178 |

| 3 | BANK OF NEW YORK MELLON CORP | 0.09533 |

| 4 | FAUQUIER BANKSHARES, INC. | 0.02143 |

| 5 | MACKINAC FINANCIAL CORP /MI/ | 0.02478 |

| 6 | CITIZENS & NORTHERN CORP | 0.05375 |

| 7 | FIRST COMMUNITY CORP /SC/ | 0.05076 |

| 8 | INVESTAR HOLDING CORP | 0.19440 |

| 9 | VILLAGE BANK & TRUST FINANCIAL CORP. | 0.13994 |

| 10 | GUARANTY FEDERAL BANCSHARES INC | 0.17724 |